This week, the total inventory of construction steel continued to decline. The total rebar inventory stood at 5.1666 million mt, down 0.36% WoW. The total wire rod inventory was 1.0759 million mt, up 1.44% WoW. On the supply side, blast furnace steel mills currently enjoy moderate profits. According to the SMM survey, there were no new blast furnace maintenance activities this week, while three blast furnaces resumed production, leading to an increase in pig iron supply levels. More blast furnaces are expected to resume production subsequently, with pig iron production continuing to rise. However, EAF steel mills are facing poor profitability. This week, one EAF mill halted production for maintenance, and three EAF mills shortened their operating hours. Nevertheless, some EAF mills in South China had previously reduced production, resulting in insufficient order fulfillment. This week, they extended their operating hours to ensure delivery. On the demand side, the off-season demand weakness persisted. Hot and rainy weather constrained downstream construction activities, with terminal procurement primarily driven by immediate needs and low speculation willingness. Overall, the fundamental performance this week showed relatively small changes compared to the previous period. The total inventory of construction steel continued to decline, but the rate of decline narrowed.

This week, the total rebar inventory was 5.1666 million mt, down 18,700 mt WoW, a decrease of 0.36% (previous value: -1.43%). Compared to the same period of the lunar calendar last year, it decreased by 217.11, a decline of 29.59% (previous value: -29.21%).

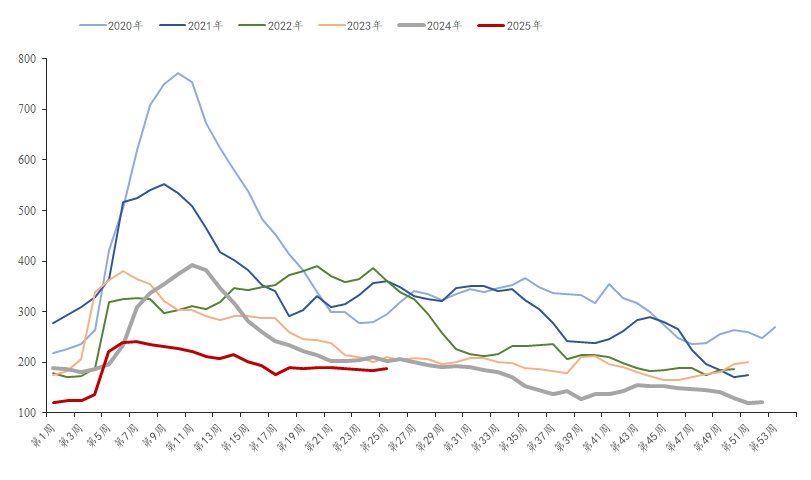

Chart-1: Overview of Rebar Inventory

Data Source: SMM

This week, the in-plant inventory of rebar was 1.8808 million mt, up 35,400 mt WoW, an increase of 1.92% (previous value: -0.80%). Compared to the same period last year, it decreased by 130,600 mt, a decline of 6.49% (previous value: -10.74%). Currently, blast furnace steel mills enjoy moderate profits, maintaining a high level of pig iron supply, with supply levels increasing. However, due to the off-season, direct supply from steel mills has declined. This week, the inventory of construction steel mills shifted from a decline to an increase.

Chart-1: Trend of Rebar Factory Warehouse Inventory from 2020 to 2025

Data Source: SMM

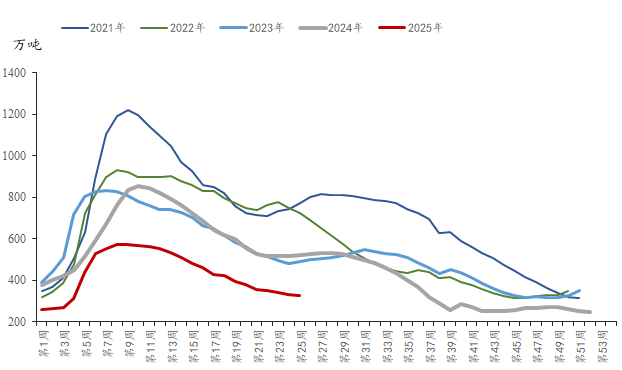

This week, the social inventory of rebar was 3.2858 million mt, down 54,100 mt WoW, a decrease of 1.62% (previous value: -1.77%). Compared to the same period last year, it decreased by 2.0405 million mt, a YoY decline of 38.31% (previous value: -36.47%). Under hot and rainy weather conditions, downstream demand remained weak, with spot prices in the doldrums. Traders maintained a cautious attitude towards the market outlook, mostly adhering to a low-inventory strategy. This week, the social inventory of construction steel continued to decline.

Chart-2: Trend of Rebar Social Inventory from 2021 to 2025

Data Source: SMM

With the continuation of hot and rainy weather, the construction steel market has entered the off-season, with overall weak demand and reduced support for prices. However, steel mills currently enjoy moderate profits, maintaining high production enthusiasm, with steel production fluctuating at highs. Overall, the current supply of building materials is increasing while demand is decreasing, making it more difficult to continue reducing the total inventory of building materials in the future. It is expected that the total inventory of building materials may shift from a decrease to an increase next week.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)